After becoming a billionnaire from his e-commerce site, Alibaba, Jack Ma, moves on to become a media mogul (see The Economist's article here). In many ways this is not too surprising. Alibaba's origins can be seen as copying Amazon (although arguably, by now, it is quite different), so maybe Mr. Ma is following Jeff Bezos' footsteps, heavily investing in media assets of 'all sorts'. The emphasis, of course, is on "all sorts" as it doesn't look like there are a lot of synergies between the various media businesses that he bought a controlling stake in. But maybe this doesn't matter.... If he looks for inspiration in the West, he will find plenty of large diversified media companies considered to be "successful".

After becoming a billionnaire from his e-commerce site, Alibaba, Jack Ma, moves on to become a media mogul (see The Economist's article here). In many ways this is not too surprising. Alibaba's origins can be seen as copying Amazon (although arguably, by now, it is quite different), so maybe Mr. Ma is following Jeff Bezos' footsteps, heavily investing in media assets of 'all sorts'. The emphasis, of course, is on "all sorts" as it doesn't look like there are a lot of synergies between the various media businesses that he bought a controlling stake in. But maybe this doesn't matter.... If he looks for inspiration in the West, he will find plenty of large diversified media companies considered to be "successful".

Monday, 14 December 2015

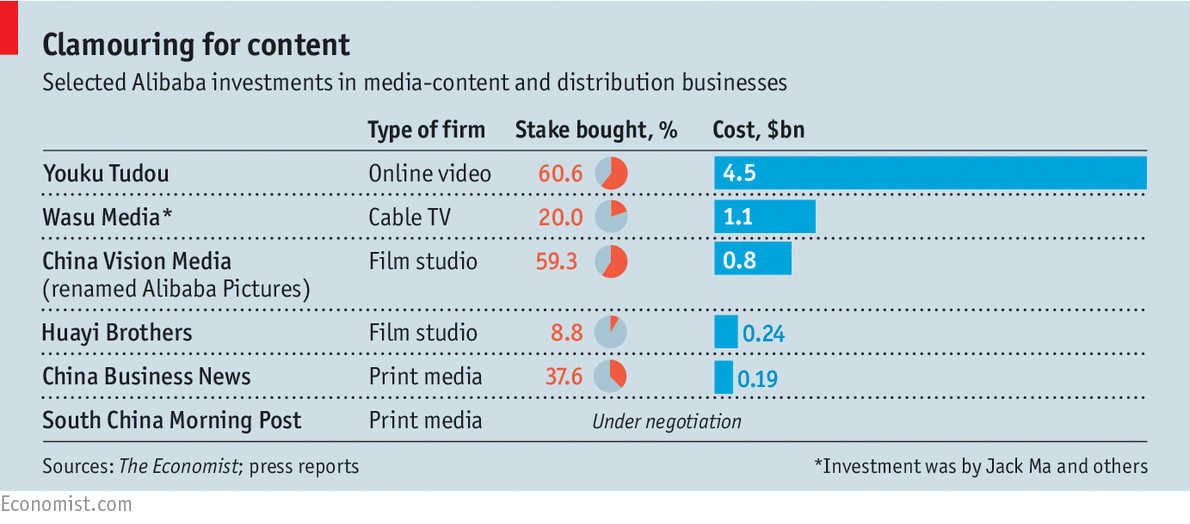

A classic "Media Mogul"

After becoming a billionnaire from his e-commerce site, Alibaba, Jack Ma, moves on to become a media mogul (see The Economist's article here). In many ways this is not too surprising. Alibaba's origins can be seen as copying Amazon (although arguably, by now, it is quite different), so maybe Mr. Ma is following Jeff Bezos' footsteps, heavily investing in media assets of 'all sorts'. The emphasis, of course, is on "all sorts" as it doesn't look like there are a lot of synergies between the various media businesses that he bought a controlling stake in. But maybe this doesn't matter.... If he looks for inspiration in the West, he will find plenty of large diversified media companies considered to be "successful".

Tuesday, 8 December 2015

WeChat's diverse use in China

WeChat, the Chinese messaging app keeps pushing the concept of social media further and further. Originally a product of Tencent designed to migrate the social network to mobile, it has eclipsed its internal competitor (the Tencent app) as well as its PC-based parent and has become a full fledged mobile social network. What is remarkable though is that - in contrast to western social media, that are still largely just entertainment platforms - WeChat integrates virtually all Internet applications, from mobile payment, to online shopping and services including even some pretty sophisticated banking products. A good summary of the crazy things that can be done on WeChat can be found here. The list drives home the point that long gone are the days when Chinese social media is just a copy of their western equivalents.

WeChat, the Chinese messaging app keeps pushing the concept of social media further and further. Originally a product of Tencent designed to migrate the social network to mobile, it has eclipsed its internal competitor (the Tencent app) as well as its PC-based parent and has become a full fledged mobile social network. What is remarkable though is that - in contrast to western social media, that are still largely just entertainment platforms - WeChat integrates virtually all Internet applications, from mobile payment, to online shopping and services including even some pretty sophisticated banking products. A good summary of the crazy things that can be done on WeChat can be found here. The list drives home the point that long gone are the days when Chinese social media is just a copy of their western equivalents.

Monday, 30 November 2015

Digital currencies

Hanna Halaburda and I have written a new book about digital currencies - it will be out at the beginning of 2016. Yes, we do talk about Bitcoin (and its many many competitors) but the book also covers, what we call "platform-based" currencies: currencies introduced and centrally managed by large digital platforms (social networks, retail platforms like Amazon or video game platforms). These have exploded in recent years and we believe that this trend will just accelerate. What might be its implications? This is what we try to answer in the book.

Hanna Halaburda and I have written a new book about digital currencies - it will be out at the beginning of 2016. Yes, we do talk about Bitcoin (and its many many competitors) but the book also covers, what we call "platform-based" currencies: currencies introduced and centrally managed by large digital platforms (social networks, retail platforms like Amazon or video game platforms). These have exploded in recent years and we believe that this trend will just accelerate. What might be its implications? This is what we try to answer in the book.And now we also have a facebook page. Check it out here.

Friday, 30 October 2015

Net neutraility in the US and the EU

Europe has just proposed its own version of net neutrality law and critics are already tearing it apart. This article from The Economist compares it to the US version and broadly concludes that the European law is looser on net neutrality than the US, which will result in less innovation on the Internet. The article claims that the main reason for this difference between the two continents comes from the fact that in Europe, the balance of lobbying power is in favour of the large infrastructure (telco) companies instead of Internet platforms. In fact, European telcos - many of which are close to the government it is claimed - find eager listeners in regulatory bodies who are tired to witness the crushing success of American Internet giants on their continent.

This view is quite superficial. First of all, I don't think that there is such a large difference across the two continents in their approaches to net neutrality: there are loopholes large enough in both laws as well as many uncertainties concerning details of implementation - The Economist ends their analysis acknowledging that the US law faces many hurdles still. Second, it is not clear that European telcos have more leverage with their governments than say AT&T (which has just managed to reassemble itself to control a large chunk of digital traffic), or say, Comcast and some other large cable networks. Third, expensive infrastructure for consumers is just as much a roadblock to innovation on the Internet than net neutrality - in fact, arguably more so. European broadband costs are much lower than equivalent service costs in the US and as a result Internet usage is way ahead in Europe compared to the US. Fourth, net neutrality is not an unambiguous good thing so that more of it is automatically better. Network management is complex and priority needs to be provided to some content to avoid congestion - finding the right balance is extremely complex. While some bandwidth needs to be guaranteed to poor new application providers, it makes sense for intense users to pay more for the infrastructure used.

Innovation on the Internet has been dismal in Europe when compared to the US. This however, does not come from overregulation of the Internet but much more from the lack of appropriate financial infrastructure and the lack an investment friendly economic environment. Indeed, the gap in innovation across the two continents is also present in other industries, not just technology.

Thursday, 8 October 2015

Adblocking on the rise

Adblocking became a real problem for advertisers last spring as the number of users installing such software rose to over 200 hundred million users across the planet (see article here). Early in the summer, I thought that this problem might matter for the long tail of content providers, largely sparing the big ad platforms (Google, Facebook, etc.). Not withstanding problems related to net neutrality, I thought that by and large the digital advertising market will remain the same as it is already concentrated in the hands of the large ad platforms.

Adblocking became a real problem for advertisers last spring as the number of users installing such software rose to over 200 hundred million users across the planet (see article here). Early in the summer, I thought that this problem might matter for the long tail of content providers, largely sparing the big ad platforms (Google, Facebook, etc.). Not withstanding problems related to net neutrality, I thought that by and large the digital advertising market will remain the same as it is already concentrated in the hands of the large ad platforms.Today, when infrastructure providers also consider adopting adbloking technology, it is clear that I couldn't have been more wrong. It is precisely the large ad platforms that might be hurt the most. Two particular events raise concerns. First, Digicel, a large mobile service operator decided to block ads on mobile phones. If other infrastucture providers follow a bitter negotiation can emerge, not unlike the one we saw emerging from time to time between cable operators and content providers (Comcast vs. Netflix or CBS vs. TWC). Such fights and the resulting settlements usually leave consumers worse off by introducing inefficieny in the market leading to high prices. The second event consists in Apple's large scale adoption of adblocking apps, some of which even block ads running within apps (e.g. Facebook's ads). Again, if a large platform like Apple blocks similarly large ad-based paltforms like Facebook and Google, then a lot of inefficiency can creep into the system.

There aren't only negative effects associated with these developments. The average quality of ads will rise partly due to the weeding out of really bad ads but also due to advertisers increased investment in ads that are relevant and impactful. Pages will load faster, a major concern for users that is driving in part the ad blocking trend. Still, adblocking may have just opened the next huge battle between large Internet platforms (just when we thought that patent wars might taper off as a result of a few reasonable settlements).

Tuesday, 29 September 2015

Contest between news providers

Here is a nice short video on the Associated Press' new website summarizing our conclusion on news industry competitive dynamics.

Monday, 31 August 2015

Google fights the EU

Google decided to put up a strong fight against the EU anti-competitive charges. See FT article here.

It will be an epic battle lasting years. Hopefully, it will not consume the company's energies the way a similar war has weakened Microsoft, that barely recovered from it if ever.

It will be an epic battle lasting years. Hopefully, it will not consume the company's energies the way a similar war has weakened Microsoft, that barely recovered from it if ever.

Friday, 21 August 2015

A busy summer

A lot happened in media this summer. First, the world has really woken up to the fact that streming is going to kick a real dent into the TV/Cable business. As a result many large media conglomerates owning TV or Cable assets saw a drop in their share price. Another interesting news is that News is back in vogue! Pearson has sold the FT to Nikkei for a nice price and The Economist has also been sold at a price comparable to that of Buzzfeed, the hot new media startup in which Comcast made an important investment. Who would have thought a couple of years ago that news (printed news) will still be alive in 2015? A lot happened on the new media/tech side as well. Google reorganized to become Alphabet to become more transparent about its diverse ventures. The bulk of the revenues still come from Google of course.... Facebook surged ahead of other social networks, LinkedIn and Twitter, in particular. It is becoming clear that the scale now matters more than what teens find sexy on social media. We will have an interesting Fall!

Wednesday, 10 June 2015

Blocking ads

Ad blocking can become a real problem for the media industry (see article from The Economist, see also this WSJ article). Ironically, I dont think it'll really affect the big advertisiers (Google, Facebook, etc.). These firms can negotiate with Adblock tech firms to pay a toll for their ads to pass. Similarly, they might be able to force consumers to look at ads: e.g. Google can deny service if adblock is installed - will people say, no I am not using Google? Not clear. On the other hand, what might happen to small sites living of advertising is not clear. In other words, Adblock might lead to an even more concentrated ad market.

Ad blocking can become a real problem for the media industry (see article from The Economist, see also this WSJ article). Ironically, I dont think it'll really affect the big advertisiers (Google, Facebook, etc.). These firms can negotiate with Adblock tech firms to pay a toll for their ads to pass. Similarly, they might be able to force consumers to look at ads: e.g. Google can deny service if adblock is installed - will people say, no I am not using Google? Not clear. On the other hand, what might happen to small sites living of advertising is not clear. In other words, Adblock might lead to an even more concentrated ad market. Friday, 5 June 2015

Credit Rating Agencies

Tuesday, 12 May 2015

Publishers on Facebook

Facebook has pretty much managed to convince publishers to put their content on its powerful platform. The value proposition is simple: Facebook knows how to sell mobile ads against that content as opposed to helpless publishers whose current revenues from mobile ads are very small. Publishers can keep 70% of the ad revenues sold by the Facebook (they can keep 100% of ad revenues they generate). For publishers, this is a substantial revenue potential, while they have no real alternative. Facebook's mobile display ad revenue share is 35%, by far the largest and still growing fast. Moreover, an overwhelming proportion of the traffic to publishers' sites already comes from Facebook (see WSJ chart), which is mostly accessed by via smartphones. If this trend holds up - as it seems to - publishers have no choice but to upload (some) of their content on Facebook.

Facebook has pretty much managed to convince publishers to put their content on its powerful platform. The value proposition is simple: Facebook knows how to sell mobile ads against that content as opposed to helpless publishers whose current revenues from mobile ads are very small. Publishers can keep 70% of the ad revenues sold by the Facebook (they can keep 100% of ad revenues they generate). For publishers, this is a substantial revenue potential, while they have no real alternative. Facebook's mobile display ad revenue share is 35%, by far the largest and still growing fast. Moreover, an overwhelming proportion of the traffic to publishers' sites already comes from Facebook (see WSJ chart), which is mostly accessed by via smartphones. If this trend holds up - as it seems to - publishers have no choice but to upload (some) of their content on Facebook. Monday, 20 April 2015

“Mobilegeddon”

This is a cool! Google re-evaluates search rankings based on whether sites are mobile friendly or not. Many will complain but this shows how this general pressure overall benefits consumers. Read more about it at this FT link.

Wednesday, 15 April 2015

Europe going crazy on Google again

Europe has decided to really go after Google by filing formal charges against the search engine (see FT article). It is quite clear that most of this is driven by politics (a former settlement was objected by finance ministers from France and Germany). The French lead the way, of course, by proposing a law whereby Google would need to hand over its proprietary algorithm to the French government so that it can check whether the search engine is fair to its rivals. This level of intervention is totally crazy. Even if one can argue that damage has been done to rival businesses, the resources dissipated in the legal process, lobbying and politics is by no means beneficial to society. To see the unreasonable lobbying that puts pressure on politicians, consider this other FT article on major music groups' attack on Google. The Internet is a fast evolving space with incredible benefits to consumers. Holding back investment and providing negative incetives for innovators is not a wise policy.

Monday, 6 April 2015

Agenda Chasing by the News

The Reynolds Journalism Institute (RJI) published a short blog on our paper with Zsolt Katona from Berkeley's Haas School of Business. It is about Agenda Setting in the News and it argues that with lower barriers to entry and lower customer switching costs agenda setting is more "Agenda Chasing" by news providers who are in a contest to become the 'go-to-place' for a particular topic.

Friday, 20 March 2015

TV disruption

Maybe the moment has come when enough pressure is built to blow up the traditional TV industry. Today's FT article nicely summarizes the many initiatives that all aim at securing a strong place in the new TV ecosystem. Interestingly, these initiatives no longer come from startups like Netflix and Hulu only. Instead, the new business-model innovatiors are Dish, Apple, Sony and HBO, in other words, traditional large companies. Another important observation is that consumers may not pay less for TV than before. When these fragmented services' fees are added up the check might be very similar to current typical cable bills ($100-$125). Consumers' choice will look very different though, which is a major improvement in terms of the overall quality of TV experience. What will definitely change is the distribution of revenues across players in the ecosystem. Cable networks - especially the small niche ones - might lose revenues. Cable providers will also lose revenues from cord cutters. Some newcomers - e.g. Apple - might win revenues. Profitability might not follow revenues though. Cable companies might actually become more profitable as their margins on Internet services is higher than the margin on the distribution of content.

Wednesday, 4 March 2015

NYC Media Seminar by Justin Rao

Thursday, 26 February 2015

Social Media Week in NYC

Monday, 23 February 2015

The oscars

And just one day after the results The Economist (see article here) does a wonderful analysis of the Oscars putting into perspective the change that slowly happened over the last 10 years and explaining why the industry has become more "open minded" in its praise. The highlights: less risk taken by big studios to create original content, more experimentation, especially by TV series and more openness for indie and foreign productions.

Thursday, 5 February 2015

New York City Media Seminar: Vertical integration

At last week's New York City Media Seminar, Greg Crawford from the University of Zurich presented a fantastic paper on vertical integration yesterday. The paper examined whether and when an integrated content owner and content distributor would foreclose their content from a rival distributor. They collected data on the availability of regional sports networks on multi channel cable and satellite services across the US. They definitely find evidence that the integrated entities tend to optimize the joint profit of the enterprise (maybe not fully but almost). Yet, for this particular content it is not obvious that this necessarily leads to foreclosure of content. This depends on the demand (consumers' willingness to pay for the content). The paper is remarkable in its treatment of institutional details - rarely seen in empirical work, especially for such a complicated problem. And, again, it shows that regulation is extremely complex for these industries.http://www8.gsb.columbia.edu/media/faculty/researchseminars

Friday, 30 January 2015

Net Neutrality

This short article in The Economist nicely concludes on the extremely complex issue of net neutrality. (A slightly more detailed report can be read here). The basic point is that precisely because it is very complex, the problem should be dealt with light regulation setting only broad guidelines and still leaving room for the market to figure out an efficient allocation. It is becoming increasingly clear that the core issue is the lack of competition for consumers to access broadband. Introducing competition would go a long way to make the net neutrality problem go away. It seems that US regulators seem to move in this direction.

This short article in The Economist nicely concludes on the extremely complex issue of net neutrality. (A slightly more detailed report can be read here). The basic point is that precisely because it is very complex, the problem should be dealt with light regulation setting only broad guidelines and still leaving room for the market to figure out an efficient allocation. It is becoming increasingly clear that the core issue is the lack of competition for consumers to access broadband. Introducing competition would go a long way to make the net neutrality problem go away. It seems that US regulators seem to move in this direction. Friday, 23 January 2015

New Editor in Chief at The Economist

The Economist has chosen a new editor and the choice boiled down to (see FT article for details) Zanny Minton Beddoes. She is the first female editor of the 150+ years old magazine that has defined adverse industry dynamics with its unique editorial model. Minton Beddoes has all the right lines on her CV to become a very successful editor. She is an economist from Oxford and Harvard, worked at the IMF and has been involved with global policy advice across the planet. She has been with the magazine for over 20 years.

The Economist has chosen a new editor and the choice boiled down to (see FT article for details) Zanny Minton Beddoes. She is the first female editor of the 150+ years old magazine that has defined adverse industry dynamics with its unique editorial model. Minton Beddoes has all the right lines on her CV to become a very successful editor. She is an economist from Oxford and Harvard, worked at the IMF and has been involved with global policy advice across the planet. She has been with the magazine for over 20 years.

Subscribe to:

Posts (Atom)